Regulatory clarity implemented this year for bitcoin and the crypto world ‘opened the doors’ for a new business profile, also involving monetary authorities and their digital currencies.

From the shock caused by the Silicon Valley bank crisis in March to the countdown for the approval of the first Bitcoin Spot ETF in the US, bitcoin’s price more than doubled in 2023. However, this surge doesn’t come from the volatile “old days” of crypto. But rather from a new context of institutional adoption of the digital asset and technology, by both investors and governments.

Greater regulatory clarity in major jurisdictions like the EU and Brazil, along with the tokenization of real assets, took the crypto ecosystem to a new level this year. And Brazil stands out as one of the leaders in this evolution.

“2023 was a year of maturation for the crypto market in Brazil and globally,” says crypto lawyer Nicole Dyskant. “We had some mishaps, but scandals were necessary to shed light where it was needed, keep bad actors away, and boost regulations around the world.”

Nicole also highlights the $4 billion settlement between Binance and the US Department of Justice, after the exchange admitted to wilfully failing to maintain anti-money laundering policies and implement preventive controls.

Heavyweights Entry

According to a Coinbase report, the number of global crypto users increased to 420 million in 2023, with significant growth in the US.

A Binance report notes that while the potential for a Bitcoin Spot ETF in the US has existed for a long time, “notable positive developments towards it becoming a reality happened this year”. There are currently 13 Bitcoin Spot ETF applications under review by the SEC.

Brazil’s Starring Role

Regulatory developments in Brazil and the adoption of crypto by local traditional financial institutions also leapt forward. The publication of the Legal Framework for Crypto Assets and Itaú offering Bitcoin on its Íon platform happened in the same context.

“Itaú’s move is a very positive one for Brazil’s digital asset market,” says BitGo’s Juliana Walenkamp. “It brings more visibility to the sector, leading to greater liquidity and capital inflow,” she adds.

According to Dynasty Global’s Eduardo Carvalho, Itaú’s market entry “represents a turning point for the crypto ecosystem”. He notes that the 2024 Bitcoin halving will likely boost assets’ value further. “Strategically, Itaú is positioning itself before this boom,” says Carvalho.

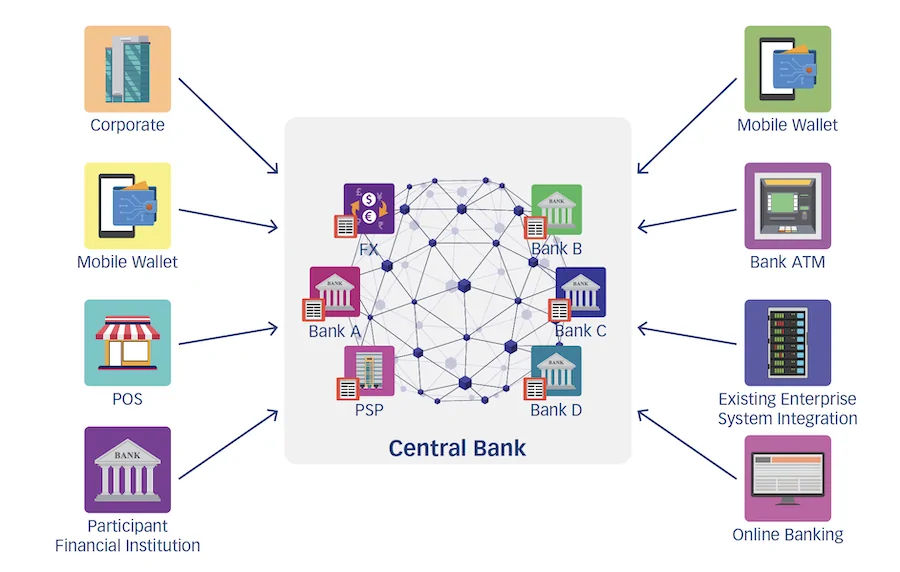

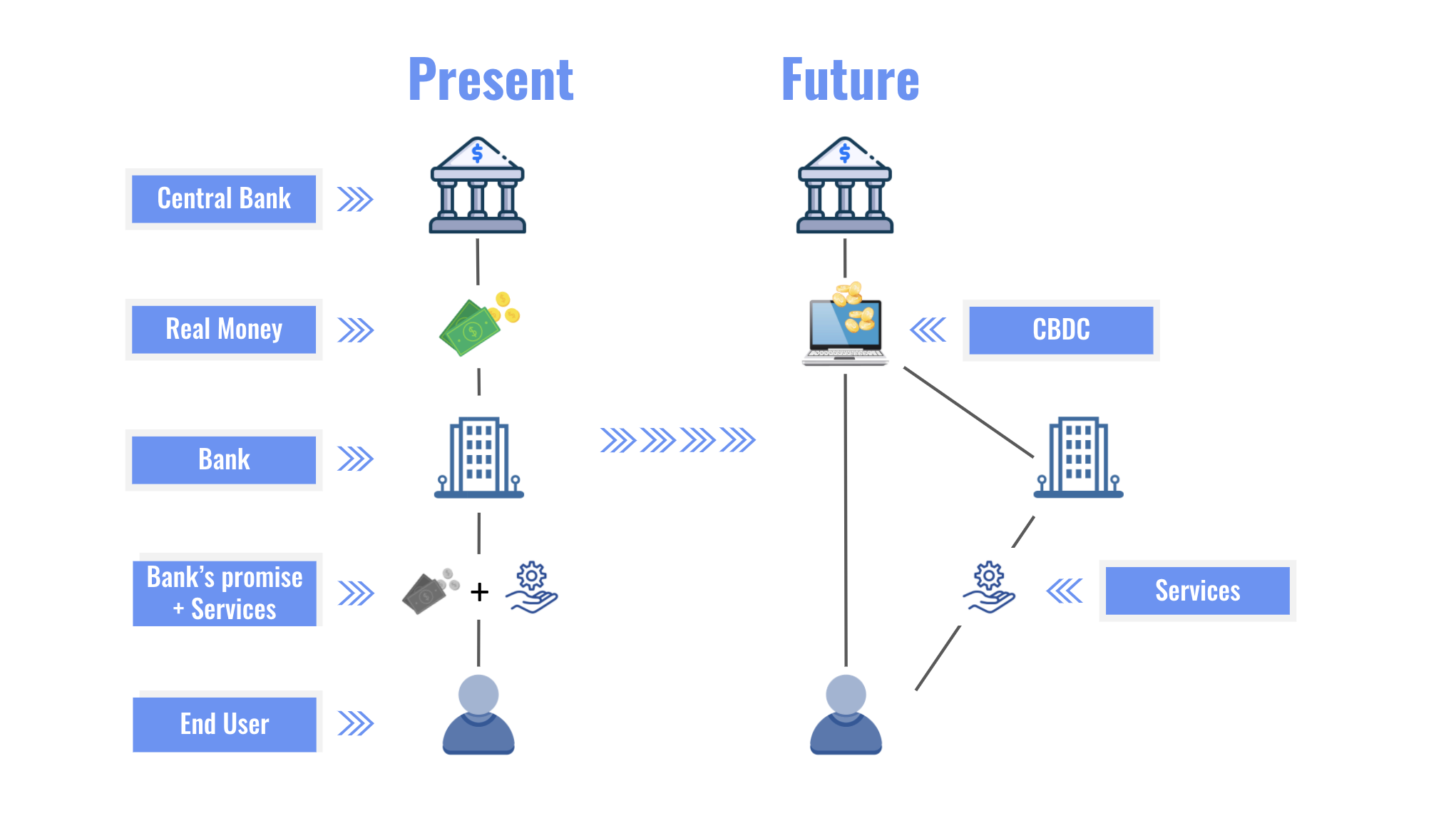

On the regulatory side, Brazil has been developing AML rules for Virtual Asset Service Providers (VASPs) since before 2023. Moreover, its central bank’s DREX CBDC project advanced brilliantly.

“Brazil became a ‘proof of concept’ of crypto regulation,” says Walenkamp. “It was one of the first countries to approve a crypto ETF and a few to greenlight multi-crypto ETFs.”

CBDCs’ Global Rise

Many central banks now have projects related to DLT, CBDCs and DeFi integrations, notes Hashdex’s Pedro Lapenta. CBDCs are also opening the door for innovative applications, says Javier Andrés from VAAS.

In 2024, this trend will gain a lot of traction. We can expect to see more countries testing or even launching CBDCs, says Andrés. The integration of CBDCs into traditional financial systems is a game changer, as they take on roles from cross-border transactions to everyday retail payments.